When a customer decides not to opt for digital bill payment, security is often the reason. Not a confusing interface. Not a technical problem. It’s an issue of trust.

For the finance manager who needs to justify a new payment platform investment, this framing matters. The ROI of PCI compliance and security posture isn’t just risk avoidance. It’s adoption. Every percentage point increase in digital payment uptake reduces the cost of paper billing, inbound call volume, and manual payment processing.

Let’s take a look at what new data says about the perception of secure digital payments on e-payment adoption, how you can signal security, how you can communicate security to your customers, and how you can evaluate the security and compliance of a payments processing solutions.

What the Data Reveals About Security and Digital Payment Adoption

Security concerns asides, most modern consumers are interested in the convenience of digital bill payment. According to the 2026 State of Online Payments report, 83% of Americans prefer to pay bills digitally. But preference and behavior are different things.

Another survey InvoiceCloud conducted with our partners at PAN Communications and Dynata shows that 55% of customers — even those who prefer digital payments — will abandon checkout when they encounter friction, unfamiliar interfaces, or anything that signals their sensitive information isn’t safe.

Furthermore, 82% from that same survey are more likely to make a bill payment on a digital platform that highlights security and compliance.

The gap between “willing to pay online” and “actually pays online” is largely a trust gap. Organizations that close it — through visible security signals, secure user authentication for staff, and PCI-certified platforms — can see higher digital adoption rates than those that treat security as a backend concern.

Advanced Identity Security: What is It and How Does It Improve Security?

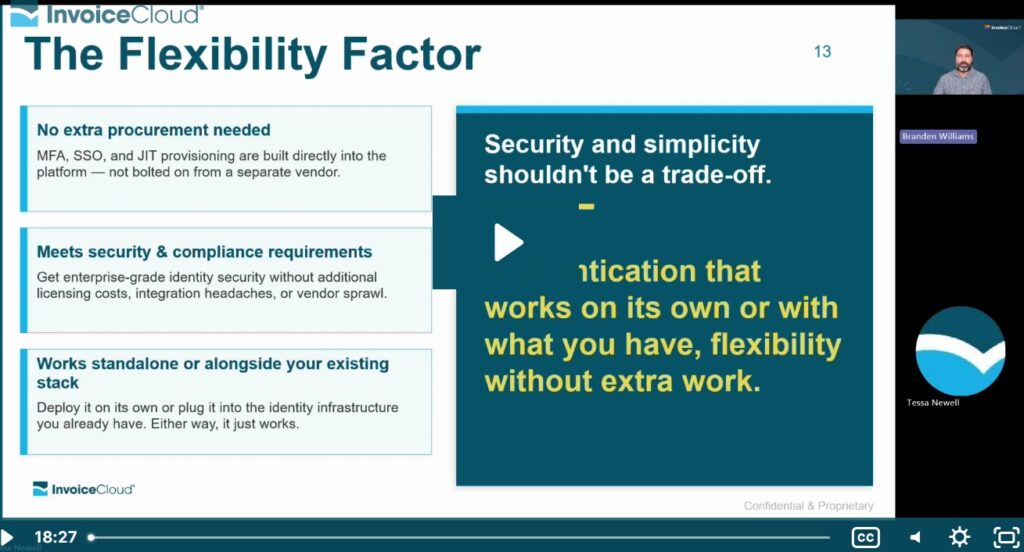

Advanced Identity Security is essentially the login and authentication experience your payers and staff interact with every time they access your portal.

These Advanced Identity layers can be built directly into a billing and payment platform, which means you don’t need to go out and source a separate identity platform to get enterprise-grade protection. Ideally, your payment platform should allow the flexibility to work on its own or with your existing tech stack.

At its core, Advanced Identity Security includes three things: support for enterprise authentication standards, built-in Multi-Factor Authentication (or MFA) and Single Sign-On (or SSO).

If you want to learn more about MFA and SSO, “Just in Time” user provisioning, and how these features keep your system secure and your staff workflows efficient, watch my episode of the Customer Confidence webinar series below.

How to Signal Security to Your Customers

As the data shows, security is just as much about customer perception as it is about the important safeguards under the hood of your payment solution. There are a few foundational signals your payers are looking for, often without even realizing it — and they apply whether you’re running online bill payment services for a utility, processing municipal payments, or collecting property tax payments on behalf of a county.

- SSL/TLS Encryption — That “https://” in the URL and the padlock icon in the browser bar. It tells your customer that data is encrypted in transit. This is table stakes, but it’s something payers actively notice and respond to.

- High-Grade Encryption— With high-grade encryption, sensitive payment data is never displayed or retrievable after submission, so customers can pay with complete confidence.

- Digital Wallets — Options like Apple Pay and Google Wallet use device-level security and are increasingly familiar and trusted by consumers. Payments without the need to key in a card number isn’t just convenient, it signals security, as well.

These features don’t just protect your customers, they reassure your customers. And reassured customers complete payments.

What Are PCI Compliant Payments?

PCI compliant payments are transactions processed in accordance with the Payment Card Industry Data Security Standard (PCI DSS), a set of technical and operational requirements developed by the major card brands — Visa, Mastercard, American Express, Discover, and JCB — to protect cardholder data.

The standard applies to any organization that stores, processes, or transmits credit or debit card data. That includes your billing vendor. If they touch card data on your behalf, their compliance posture is your compliance posture.

Compliance often gets framed as a burden, something you have to do. But let’s reframe it: compliance is also a customer benefit.

When your payment platform is PCI DSS compliant, when it meets accessibility standards, when it checks the boxes your regulators require — that’s not just protecting your organization. That’s making your platform safer and easier to use for every single one of your payers.

This matters especially for organizations managing online utility bill payment, online property tax payments, or government payment solutions at scale. For municipalities and counties pursuing billing modernization, the PCI DSS security standards your payment processing solution is built on determine not just your audit posture, but your residents’ willingness to pay digitally.

Accessibility in particular is worth calling out. If you want to do a deep dive on this, I highly suggest watching the first episode of our Customer Confidence webinar series, all about how to ensure your payment platform is accessible.

How to Communicate Security to Customers

Okay, so you have the security infrastructure. You have the compliance certifications. Now what?

One of the most common missed opportunities we see is billers who have done tremendous work on the security side of their platform, but haven’t built the customer-facing communications to go with it. Here are a few ways to communicate the security of your payments system to worried customers:

- Have materials ready: FAQs, help center content, email communications, even simple on-screen messaging that explains to your customers what you’re doing to protect them.

- Promote best practices: It doesn’t hurt to regularly share best practices with your customer base, like ways to keep their passwords secure. Not only does this serve to keep everyone safer, it further solidifies to your customers that your organization is security-minded and has their best interests at heart.

This kind of proactive communication does two things: it demonstrates your commitment to security, and it gives customers confidence that you’re a partner they can trust. That trust translates directly to adoption.

At InvoiceCloud, we have a dedicated marketing team for our customers. The team helps them by creating materials like these to communicate important messages to their customers: like how to self-serve or how we ensure their financial information is secure.

Checklist: Evaluate a Vendor’s Security and PCI Compliance Credentials

Asking a vendor if they’re PCI compliant or secure isn’t enough. That’s why we created a checklist that compiles all the things you should ask your current or prospective payment vendor. Any good payment solution will welcome these kinds of questions:

- Do they hold Level 1 certification — the highest tier? Can they provide documentation?

- Do they maintain SOC 1 and SOC 2 Type 2 certifications, verified by an independent auditing firm?

- Do they provide a Trust Center upon request that’s actively maintained and up to date?

- Do they offer Advanced Identity Security options like MFA, SSO, and JIT?

For a structured evaluation process, get the checklist to bring into vendor conversations.

Frequently Asked Questions

What is the penalty for PCI non-compliance, and how are fees assessed?

Card brands can assess monthly fines between $5,000 and $100,000 on acquiring banks for non-compliant merchants or service providers. Those costs are typically passed through to the non-compliant party. Fines continue until compliance is demonstrated — they don’t resolve with a single payment.

Is PCI compliance legally required, or is it a voluntary standard?

PCI DSS is not a federal law in the United States, but it is contractually required by the card brands as a condition of accepting card payments. Some states have incorporated PCI DSS requirements into data security legislation, and regulators in some industries reference it as an expected standard of care. For most organizations, non-compliance creates both contractual and legal exposure.

Does using a certified payment processor mean your organization is automatically PCI compliant?

No. Your processor’s compliance reduces the scope of your obligations, but it doesn’t eliminate them. If you store, transmit, or have any system access to cardholder data — even temporarily — you have compliance responsibilities independent of your processor. This is one of the most common misconceptions in vendor compliance conversations.

How does PCI compliance affect customer trust and digital payment adoption?

The relationship is direct. Customers who see visible security signals — SSL indicators, recognizable payment interfaces, MFA prompts — are more likely to complete a digital payment transaction. Organizations with PCI-certified platforms and strong authentication infrastructure consistently see higher digital adoption rates than those where security is less visible or documented.

What should you look for when evaluating a PCI compliant payment vendor?

Current ROC or SAQ documentation, recent ASV scan results, a QSA-signed Attestation of Compliance, clear scope definition, and a documented incident response history. The checklist above covers each criterion in detail.